|

Amortization Methods |

|

Navigation: Loans > Loan Screens > Insurance Screen Group > Policy Detail Screen > Policy Information tab > Insurance Information field group >

Amortization Methods

|

Amortization Methods |

|

Use the Amortization Method field to indicate the method used for amortizing a portion of the original insurance premium each month. Any amount that is unearned when the policy is cancelled or paid off is refunded back to the borrower (depending on the amount of the refund and whether other options exist on the Insurance Information field group, such as Min Refund Amount or Do Not Refund).

All amortization methods will use an adjusted effective date if the Use Anniversary of 1st Due Date field is marked. The adjusted effective date is used for determining the starting date for refunding. It may also be used for determining the remaining term.

Possible selections in this field are as follows. Click the description (or scroll down) to view more detailed information about each method.

Code |

Description |

|---|---|

1 |

|

2 |

|

3 |

|

4 |

|

5 |

|

6 |

|

7 |

|

8 |

|

9 |

|

10 |

|

11 |

|

12 |

|

13 |

|

14 |

|

15 |

|

16 |

|

17 |

|

18 |

|

19 |

|

20 |

|

21 |

|

23 |

|

24 |

|

25 |

Amortization Method |

Description |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Original Premium * Remaining Term / Policy Term = Unearned Premium

Original Premium - Unearned Premium = Earned Premium

Example: The original premium amount to be amortized is $1,550.00. The policy term is 60 months, the beginning of the amortization period (amortization start date) is 12-01-05, and the remaining term is 58 months.

The calculation is:

1550.00 * 58 / 60 = 1498.33 Refund (unearned premium) 1550.00 - 1498.33 = 51.67 (earned premium)

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Original Premium * (Remaining Term * Remaining Term + 1)) / (Policy Term * (Policy Term + 1)) = Unearned Premium

Original Premium - Unearned Premium = Earned Premium

Example: The original premium amount to be amortized is 1550.00. The term is 60 months, the beginning date is 12-01-01, and the remaining term is 58 months. The calculation is:

1550.00 * (58 * 59) / (60 * 61) = 1449.21 Refund (unearned premium)

1550.00 - 1449.21 = 100.79 (earned premium) |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Two different formulas are used when calculating the rule of anticipation amortization.

One formula uses a state rate and the premium received to calculate the amortization.

The other formula is based on Premium Rate Tables. If you have a valid table number in the Premium Rate field, the second formula is used. Otherwise, the first formula is used and the State Rate and Premium Received fields become required for the amortization calculation.

Formula 1 (State Rate * Remaining Term) / 1200 = Re-Rate %

(Original Premium - (Period Payment * Months Into Term)) * Re-Rate % = Re-Rated Premium

Original Premium * State Rate % * Policy Term in Years = Re-Rated Premium

Re-Rated Premium / Original Benefit * Premium Received = Unearned Premium

Original Premium - Unearned Premium = Earned Premium

Example: The state rate is .5600. The premium received is 298.92 and the period payment is 493.79. The original term is 36 months, and the remaining term is 31 months. The original premium is 17,776.44. The beginning date is 09-01-01. The calculation is:

(.5600 * 31) / 1200 = .014467 (re-rate%) 17,776.44 - (493.79 x 5) = 15,307.49 (remaining benefit) 15,307.49 * .014467 = 221.45 (re-rated premium) (17,776.44 * .0056) x 3 = 298.64 (original premium) 221.45 / 298.64 * 298.92 = 221.66 (refund to borrower)

Formula 2 Original Premium * (Rate for Remaining Term * Remaining Term) / (Rate for Policy Term * Policy Term) = Unearned Premium

Original Premium - Unearned Premium = Earned Premium

The rate for remaining term and rate for policy term are pulled from the Premium Rate Table. The Premium Rate Table is set up by GOLDPoint Systems in Blue WinTerm. See the Rule of Anticipation Fields field group for more fields applicable to this amortization method. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

(Pro-Rata + Rules of 78) / 2 = Unearned Premium

Original Premium - Unearned Premium = Earned Premium

Example: The original term is 60 months, and the remaining term is 58 months. The original premium is 1550.00.

(58 / 60) * 1550.00 = 1498.33 (pro-rata refund) 1550.00 * (58/2 + (58 + 1)) / (60/2 + (60 + 1)) = 1449.21 (rule of 78 refund) (1449.21 + 1498.33) / 2 = 1473.77 (unearned premium) 1550.00 - 1473.77 = 76.23 (earned premium) |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

I = Interest rate / 12 N = Number of months in loan term M = Number of months in insurance term T = Number of months elapsed from amortization start date to refund date

Present Value Formula at N months = (1 - (1 / (1 + I)) ^ N) / I Present Value Formula at (N - T) months = (1 - (1 / (1 + I)) ^ (N - T)) / I Present Value Formula at (N - M) months = (1 - (1 / (1 + I)) ^ (N - M)) / I

Unearned Premium = Original Premium * (Remaining Term - Present Value Formula at (N - T) months - Present Value Formula at (N - M) months) / (Insurance Term - Present Value Formula at N months - Present Value Formula at (N - M) months)

Earned Premium = Original Premium - Unearned Premium

Note: This calculation uses the Original Maturity Term field (MLOTRM) if it contains a value. If it is blank, the Loan Term field (LNTERM) is used.

Example: The original premium is 200.00. The remaining term is 57 months. The elapsed term is three months. The interest rate is 25%. The loan term is 60 months and the insurance term is 60 months.

I = .020833 N = 60 M = 60 T = 3

Present Value Formula at N months = (1 - (1 / (1 + .020833)) ^ 60) / .020833 = 34.0702863

Present Value Formula at (N - T) months = (1 - (1 / (1 + .020833)) ^ 57) / .020833 = 33.1813811

Present Value Formula at (N - M) months = (1 - (1 / (1 + .020833)) ^ 0) / .020833 = 0

Unearned Premium = 200.00 * (57 - 33.1813811 - 0) / (60 - 34.0702863 - 0) = 183.716791 = 183.72

Earned Premium = 200.00 - 183.72 = 16.28 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

I = Interest rate / 12 N = Number of months in loan term M = Number of months in insurance term T = Number of months elapsed from amortization start date to refund date

Present Value Formula at N months = (1 - (1 / (1 + I)) ^ N) / I

Present Value Formula at (N - T) months = (1 - (1 / (1 + I)) ^ (N - T)) / I

Present Value Formula at (N - M) months = (1 - (1 / (1 + I)) ^ (N - M)) / I

Unearned Premium = Original Premium * (Remaining Term * (Insurance Term + 1)) / ((Remaining Term + 1) * Insurance Term) * (Remaining Term - Present Value Formula at (N - T) months - Present Value Formula at (N - M) months) / (Insurance Term - Present Value Formula at N months - Present Value Formula at (N - M) months)

Earned Premium = Original Premium - Unearned Premium

Note: This calculation uses the Original Maturity Term field (MLOTRM) if it contains a value. If it is blank, the Loan Term field (LNTERM) is used.

Example: The original premium is 20.07. The remaining term is 10 months. The elapsed term is eight months. The interest rate is 39.97%. The loan term is 18 months and the insurance term is 18 months.

I = .033308 N = 18 M = 18 T = 8

Present Value Formula at N months = (1 - (1 / (1 + .033308)) ^ 18) / .033308 = 13.376577

Present Value Formula at (N - T) months = (1 - (1 / (1 + .033308)) ^ 10) / .033308 = 8.387971

Present Value Formula at (N - M) months = (1 - (1 / (1 + .033308)) ^ 0) / .033308 = 0

Unearned Premium = 20.07 * (10 * 19) / (11 *18) * (10 - 8.387971- 0) / (18 - 13.376577 - 0) = 6.71

Earned Premium = 20.07 - 6.71 = 13.36 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

The short rate factor reflects initial policy writing expense. The formula to generate the short rate table for each period is as follows:

D = Number of day in force T = Term of policy in years (example: T = 0.75 for nine-month term) E = Earned premium factor I = Initial policy writing expense

Example: The original premium is $100.00. The number of days in force is 26 and the original term is 1 year.

Since the number of days is 26, the value for I is (b) 10.11950.

Retain Factor: 0.17243 Refund Factor: 0.82757

Retain Amount: $17.24 Refund Amount: $82.76 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

A>(M-1) = Present Value Formula at M - 1 months A>(M-1-T) = Present Value Formula at M - 1 - T months

Refund =

OP X 1+A>(M-1-T) - [[(1+J) x ((1+I)M-T - (1+J)M-T)] / [(1+I)N-T x (1+J)M-T x (I-J)]] -------------------------------------------------------------------------------------------------------------------- 1+A>(M-1) - [[(1+J) x ((1+I)M - (1+J)M)] / [(1+I)N x (1+J)M x (I-J)]]

Note: This calculation uses the Original Maturity Term field (MLOTRM) if it contains a value. If it is blank, the Loan Term field (LNTERM) is used. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Refund = Premium x P

12 - Month Refund Table

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

This method uses the same calculation as method 1 but adds one month to the remaining months. This causes it to lag one month behind.

This method will not create a remaining month that is greater than the original term of insurance. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

This method uses the same calculation as method 2 but adds one month to the remaining months to create a one-month lag.

This method will not create a remaining month that is greater than the original term of insurance. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

NDAYS = original term of loan in months UDAYS = unexpired days P = insurance premium R = rate REFD = refund R = UDAYS / NDAYS

REFD = P x R |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Information coming soon. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

J = .0044

---------------------- (1 + J)M

VM-T = 1 ------------------ (1 + J)(M-T)

A > M@J = 1 – (1/(1 + J))M ------------------------- J

A >(M – T)@J = 1 – (1/(1 + J))(M-T) ---------------------------------- J

Refund = OP x (N – T) – (N – M) * V(M - T) – A>(M – T)@J ----------------------------------------------------------------- N – (N – M) * V(M) – A>M@J |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Using this method, the system takes 100% of the Unearned Amount and Remaining Amount (for commissions, finance charges, and taxes) fields at monthend after the insurance policy has been opened and credits it to your institution's applicable G/L account. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

This method calculates the remaining term by subtracting the number of installments (LNINNO) made from the original term, then performs a straight-line calculation (Original Premium * Remaining Term / Policy Term = Unearned Premium). |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

(Original Premium * Remaining Term / Policy Term ٭ 90% = Unearned Premium)

This method functions the same as method 1 (Straight Line / Pro Rate) except that at payoff or cancellation, the refund will be multiplied by 90% before it is given to the customer. This can be used for both the premiums and commissions. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

To use this method: •The insurance premium amortization method (INAMOR) must be 18. •The policy effective date (INOPND) and the amortization start date (INDLAC) should be the same as the date the loan was opened (LNOPND). •The policy term (INTERM) should be the same as the original loan term (LNTRMO).

This is how the premium is amortized:

•Zero months are earned from the date opened (LNOPND) to (not including) the first anniversary of the date opened (date opened plus one month). •One month is earned from the first anniversary of the date opened to the first due date (LN1DUE). •Two months are earned from the first due date through the second anniversary of the date opened. •Thereafter, another month is earned from each anniversary + one day through the next anniversary.

The months earned are used to calculate the remaining term for the Rule of 78s calculation. The remaining term (RTERM) is equal to the original term (OTERM) minus the earned or elapsed months (ETERM).

RTERM = OTERM - ETERM

RTERM cannot be negative.

Example:

Months Earned

If the loan was opened after the 28th day of the month, the anniversary of the date opened is adjusted based on the day of the date opened or the end of the month, whichever is less. Loans opened on February 28th will use the 28th as the anniversary date; not the monthend date. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

This amortization method, 19 - Pro Rata Daily / 90% Refund (INAMOR), functions similarly to Amortization Method 12 - Pro Rata Daily, except at payoff the borrower receives 90 percent of the insurance refund amount and your institution retains 10 percent.

The following calculation explains how this method is calculated:

REFD = P x R * 90%

where:

R = UDAYS / NDAYS NDAYS = original term of policy in months (Policy Term field (INTERM)) UDAYS = unexpired days of insurance policy (Remaining field (INWRTERM)) P = insurance premium (Original Premium field (INOBAL)) REFD = refund (Unearned Premium field (INWUAMT))

Example: A borrower has an insurance policy with a term of 12 months (360 days). Eight months have elapsed since the policy was opened, leaving four months (120 days) remaining on the policy. The amount of the original premium for this insurance policy was $350.

The refund in the above scenario is calculated this way:

120 / 360 = .33

$350 X .33 * 90% = $105 (This is the amount that would be refunded to the borrower.) |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Rule of Anticipation #4 (method 20) is calculated using the following formula:

Original Payment * Remaining Term * Rate (remaining term) / 100 = Refund Amount

where:

Original Payment = Original P/I Constant (LNOPIC) Remaining Term = Calculated using the effective date of the policy (INOPND) Rate = Premium Rate Tables (one for IUI and one for A&H) to be created by GOLDPoint Systems using rates your institution provides for us.

Example

An account has an Original P/I Constant of $131.34. The insurance policy is using the new Amortization Method (20 - Rule of Anticipation #4). The Remaining Term is 4. The Premium Rate Table determines that the Rate for Remaining Term is 1.45.

Original Payment * Remaining Term * Rate for Remaining Term / 100 = Refund Amount

131.34 * 4 * 1.45 / 100 = $7.62 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

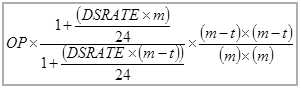

OP = original premium (INOBAL)

Refund =

Refund = INOBAL * [(1+ ((INRATE*INTERM)/24)) / (1+((INRATE*(INTERM-(refund date-INOPND))/24))]*[(INTERM-(refund date-INOPND))* (INTERM-(refund date-INOPND)) /(INTERM*INTERM)]

Please note that when setting up this method, you must also enter the correct State Rate (INRATE) of the accompanying policy. The State Rate is entered on the Miscellaneous Fields tab of the Policy Detail screen. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Use this method if your institution refunds GAP premiums based on a daily prorate, restricted to a refund base of 1095 days or less. This method is based on a calculation where:

INOPND – Policy Open Date LNOINO – Original Installment Number LNFRQO – Original Frequency INOBAL – Original Premium INTBLN – Premium Rate Table (used for 1095 day restriction) INRULE – Valid for rule 0

Calculation Steps:

1.First determine total days based on the loan original frequency and the original installment number. If the value calculated is greater than the number in INTBLN, the totals days should be the value in INTBLN (i.e. 1095). If LNFRQO is blank, use LNFREQ. For monthly, LNOINO or LNTRMO can be used. The number of days should be calculated as follows:

If LNFRQO = 1, then LNOINO * 30.42 If LNFRQO = 24, then LNOINO * 15.21 If LNFRQO = 26, then LNOINO * 14 If LNFRQO = 52, then LNOINO * 7

2.Calculate the number of days elapsed from the policy open date (INOPND) to the current date (today()) or the payoff date.

3.Subtract the days number of days from step 1 from step 2. If the value in step 2 is greater than step 1, the number of days is zero (i.e. 1095 (step 1) minus 1100 (step 2) would be 0 because 1100 is greater than 1095.

4.Take the value in step 3 and divide it by step 1.

5.Take INOBAL and times by step 4 to calculate pro rata refund.

For example:

INOBAL = 800.00 LNFRQO = 26 LNOINO = 98 INTBLN = 1095 INOPND = 1/5/2013 Cancel Date = 10/18/2014

Step 1: 98 (LNOINO) * 14 (Bi-weekly frequency value) = 1372 (Total Days) Since 1372 is greater than 1095 (INTBLN), used 1095 for days Step 2: 10/18/2014 (cancel date) – 1/5/2013 (INOPND) = 651 days elapsed (365 basis) Step 3: 1095 (step 1) – 651 (step 2) = 444 Step 4: 444 (step 3)/1095 (step 1) = 40.55% Step 5: 800.00 (INOBAL) * 40.55% (step 4) = 324.38 refund |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

This method calculates the number of days in force by taking the days difference between the policy effective date (INOPND) and the payoff date. The following table is searched to find the earned factor based on the days in force and the insurance term.

1 – Earned Factor = Unearned Factor

Original Premium * Unearned Factor = Refund (Rounded to nearest dollar)

Example: The original premium is $1200.00. The number of days in force is 136 (days difference between 09/01/2015 and 01/15/2016) The term is 12 months. The earned factor from the table is .61.

1 - .61 = .39 (Unearned factor)

1200.00 * .39 (Unearned factor) = 468.00 (Refund) |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

(Remaining Term * Remaining Term + 1)) / (Policy Term * (Policy Term + 1)) = Unearned Factor (Rounded to 3 decimals)

1 – Rule of 78s Factor (Rounded to 3 decimals) = Earned Factor

Original Premium * Earned Factor = Earned Premium

Earned Premium + .50 = Earned Premium

Original Premium - Earned Premium = Unearned Premium

Example: The original premium amount to be amortized is 1200.00. The term is 12 months, the beginning date is 09-01-15, and the remaining term is 7 months. The calculation is:

(7 * 8) / (12 * 13) = .359 Unearned Factor

1 - .359 (Unearned Factor) = .641 (Earned Factor)

1200.00 * .641 (Earned Factor) + .50 = 769.00 (Earned Premium)

1200.00 – 769.00 = 431.00 (Unearned premium) |